Major confectionery brands are rushing to capitalise on the growing consumer demand for protein. Mars, for example, has recently debuted bars and whey protein powders under the Mars Bar, Snickers and other brands, all designed to taste like the original confectionery. American confectionery giant Hershey is now taking the same path.

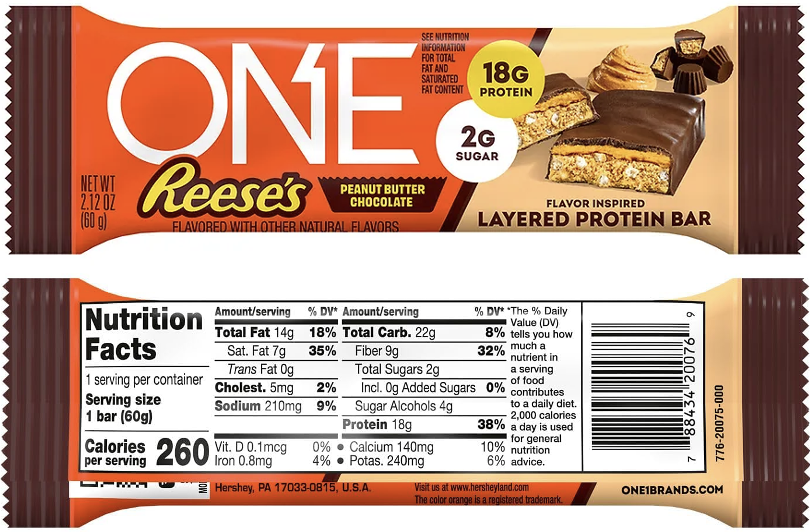

The Hershey Company in June 2026 launched ONE x Reese’s Peanut Butter Chocolate Flavoured Layered Protein Bar, a new variant under the 100 year-old Reese's brand. Reese's is one of Hershey's biggest brands, with annual retail sales of around $3.1 billion. Reese's is something of a cultural icon in the US with a continuous pipeline of innovation in flavours and texture. Initially available through Amazon, the new Reese's protein bar is expected to expand into nationwide retail channels in late 2026.

Hershey says the new bar aims to combine health benefits with an indulgent taste experience and satisfying texture from combining peanut butter and chocolate in a layered product. Each 60g bar delivers:

-

18g of protein from peanuts, whey protein isolate and milk protein isolate

-

9g of fibre from soluble corn fibre and nuts

-

Only 2g of sugar, with sweetness provided by sucralose

The high protein, fibre and low sugar profile creates a permissible indulgence which should have wide consumer appeal. It also will appeal to people using GLP-1 medications, meeting their nutrition expectations around snacking. Hershey makes no reference to GLP-1 in communications for the new bar, but its nutritional profile should resonate with informed, label-reading GLP-1 consumers.